TL;DR: Shopify Plus includes basic net payment terms but cannot enforce credit limits at checkout, track payment due dates, or generate invoices automatically. Merchants who built proper net terms infrastructure saw 38% more new buyer acquisition on average (Balance, 2025). This guide covers the six payment capabilities your B2B store needs, how to architect them on Shopify Plus, and what breaks when you skip the work.

Shopify Plus supports net payment terms natively, but only at the surface level. You can assign Net 30, Net 60, or Net 90 to a company location and the buyer will see that option at checkout. What Shopify cannot do is check whether that buyer has $40,000 outstanding on a $25,000 credit limit before letting the order through. It cannot send a payment reminder when the invoice is three days from due. It cannot block a new order until an overdue balance clears. Those are the capabilities that B2B commerce runs on, and Shopify Plus does not ship them out of the box.

This gap matters more than most merchants realize until they are already at scale. Early in a B2B launch, the missing pieces are manageable: finance reconciles invoices manually, sales reps track credit in spreadsheets, and the operations team approves orders through email. Then order volume grows, the buyer count doubles, and the manual infrastructure breaks. By that point, building the right payment term logic becomes a reactive fire drill rather than a deliberate design decision.

This post covers exactly what Shopify Plus gives you, what it does not, and how to architect the missing infrastructure: credit limit enforcement at checkout, due date tracking, automated invoice generation, PO workflows, buyer portal access, and ERP sync. All of it can be built on Shopify Plus without switching platforms, but it requires intentional planning, not a late bolt-on. For a broader look at what Shopify Plus can support at enterprise scale, see Shopify Plus as an enterprise ecommerce platform.

Why B2B Payment Terms Are Infrastructure, Not a Checkout Option

In consumer ecommerce, payment is a transaction endpoint. The buyer enters a card number and the purchase closes. In B2B, payment is a relationship mechanism. Net 30 is not just “pay later.” It signals that the supplier trusts the buyer’s creditworthiness, reflects the terms negotiated based on purchasing volume, and affects both parties’ cash flow planning. Strip that out and replace it with a card form, and you have not simplified payment. You have broken how B2B procurement actually works.

Procurement teams at companies with $10 million or more in annual purchasing are not configured to pay by card on delivery. Their accounts payable systems require PO numbers. Their finance workflows run on net terms cycles. Their approval processes are structured around invoices, not card authorizations. If your Shopify store cannot match those expectations, they place orders with a competitor whose purchasing process fits their workflow. This is not a preference problem; it is a structural one.

The revenue impact of getting this right is substantial. According to The B2B Payments Report 2025 by Balance, merchants who introduced net terms and invoicing saw 38% more new buyer acquisition on average. Among existing customers who received trade credit access, 40% increased their monthly spend. The mechanism behind both numbers is the same: B2B buyers consolidate purchasing with suppliers whose financial workflows match their own. A supplier that forces card payment gets smaller, less frequent orders. A supplier that extends terms earns a place on the approved vendor list and receives the recurring purchase orders.

What Shopify Plus Provides Natively (and Where It Stops)

Shopify Plus has expanded its B2B feature set meaningfully since 2022. Company profiles, location-level pricing, customer-specific catalogs, and payment terms assignment are all native now. For a merchant launching a small B2B program alongside a D2C store, these features are enough. For a company running a dedicated B2B channel with hundreds of accounts, variable credit exposure, and complex order approval requirements, the native feature set runs out quickly.

What Shopify Plus B2B Includes Out of the Box

The current native B2B capabilities in Shopify Plus cover: company profiles with multiple locations and buyer contacts, payment terms assignment at the company location level (Net 15, Net 30, Net 60, Net 90, and due on receipt), customer-specific price lists and product catalogs, checkout that surfaces assigned terms as a payment option, draft orders for manual invoice creation, and a basic order history view in the customer account area. These are solid building blocks, and for straightforward use cases they perform well.

Where the Native Features End

Shopify Plus assigns terms at the company location level, meaning every order from a given buyer gets the same terms regardless of order size, product mix, or outstanding balance. The assignment is static. There is no logic layer that reads the buyer’s current credit exposure and adjusts what options are available. The platform treats net terms as a payment method label, not as a dynamic financial instrument tied to the buyer’s account status.

This creates four gaps that consistently cause operational pain at any serious B2B volume. First, there is no credit limit enforcement at checkout: a buyer who has exhausted their approved credit can place a new order on terms with no friction. Second, there is no due date tracking: once an order is placed on Net 30, Shopify has no record of when payment is due or whether it arrived. Third, there is no automated invoice generation in a format that a buyer’s AP system can process without editing. Fourth, there is no support for variable payment structures such as milestone billing or installment plans, which are standard in industrial and capital goods B2B.

Draft Orders Are Not a Scalable Substitute

Many Shopify Plus merchants rely on draft orders as a workaround: an internal team member creates the order manually, adds terms, generates an invoice PDF, and emails it to the buyer. This works for low-volume programs. At 100 or more B2B orders per month, it becomes a bottleneck. Every draft order requires human intervention. Invoice formatting is inconsistent. Payment tracking is manual. Credit checks are remembered, not enforced. And the buyer experience is slower and less self-service than they expect from a modern supplier portal. Draft orders are a starting point, not a destination.

The Six B2B Payment Capabilities Your Shopify Plus Store Needs

Building a functional B2B payment system on Shopify Plus means engineering the capabilities the platform does not ship. The six listed below cover the full range of what enterprise B2B buyers expect. Not every store needs all six on day one, but the first three represent the minimum viable infrastructure for any merchant with more than 50 active B2B accounts and variable credit exposure.

1. Real-Time Credit Limit Enforcement at Checkout

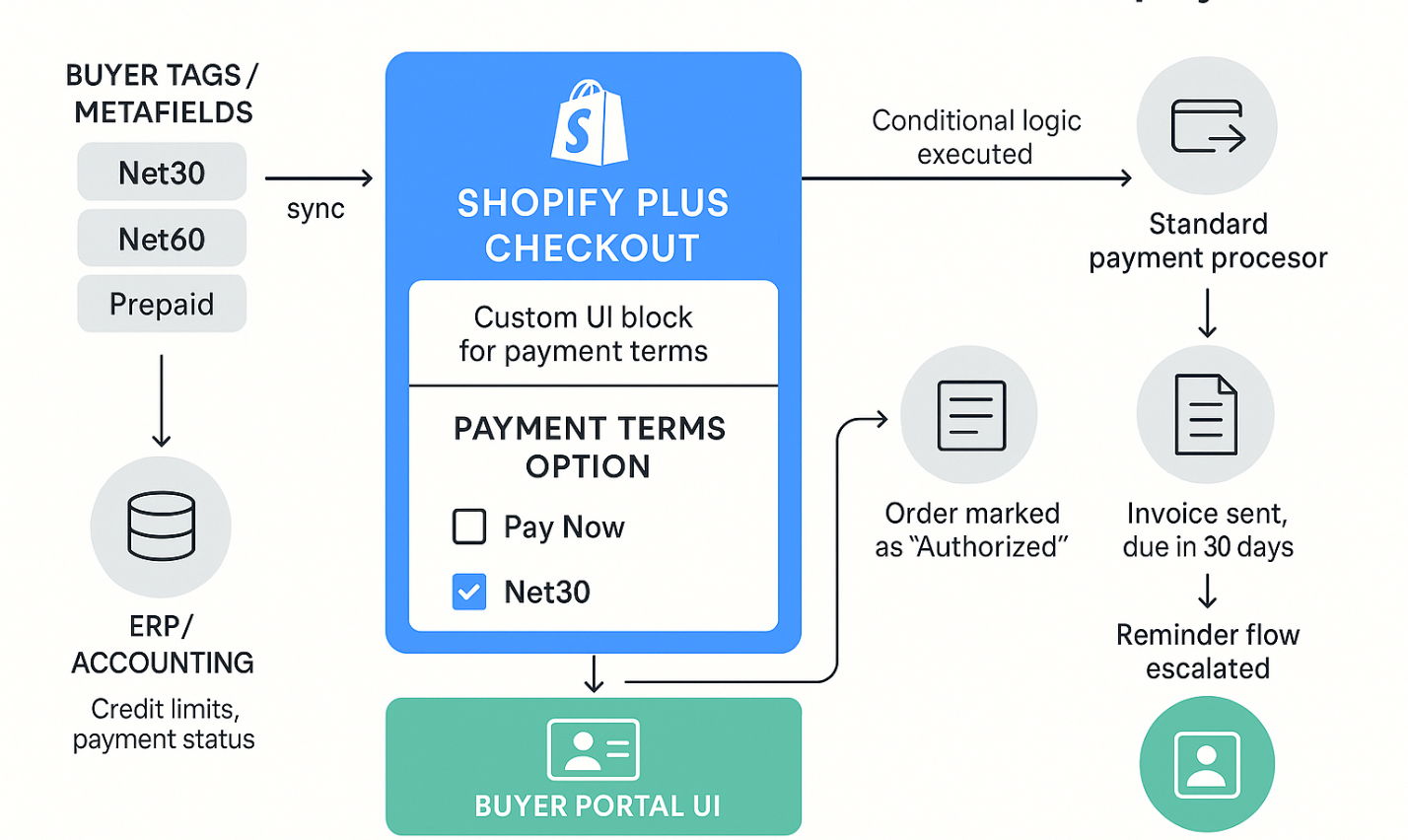

Credit limit enforcement means the checkout knows, at the moment of order submission, how much outstanding balance the buyer carries and whether adding the current cart would push them past their approved limit. Building this requires two metafields on each company location: the approved credit limit and the current outstanding balance. The balance updates via webhook from your ERP or accounting system every time a payment posts or a new order confirms. At checkout, a Shopify Function reads these metafields and hides or disables the terms payment option if the cart total would exceed available credit. The buyer sees an informative message rather than a declined order with no explanation.

2. Net Terms With Due Date Tracking and Automated Reminders

When an order is placed on Net 30, a payment due date 30 days from order creation should be written to an order metafield immediately. That date drives everything downstream: automated reminder emails (7 days out, 3 days out, day of), ERP invoice aging, and credit hold logic. Without the due date stored in a queryable field, every downstream process has to recalculate it from scratch or rely on a human to remember. The reminder workflow runs through Shopify Flow or a custom app that reads the due date metafield and triggers a notification sequence through your email platform of record.

3. Purchase Order-Based Checkout Workflows

Enterprise buyers generate a PO first, then submit the order with the PO number as a reference. Your Shopify Plus checkout needs a PO number field visible to B2B buyers, stored in order attributes or metafields, and synced to the ERP. The PO number is how the buyer’s AP team matches your invoice to their approved spend. Without it, your invoice arrives in their system with no match, gets flagged as unverified, and payment is delayed weeks. The field is simple to add via a checkout extension; the discipline is requiring it for all B2B accounts and making it optional or hidden for D2C buyers on the same store.

4. Automated Invoice Generation With Proper Formatting

An invoice requires: a unique invoice number, seller address and tax ID, buyer billing address, line-item breakdown with SKUs and quantities, applicable tax calculation, payment due date, and remittance instructions. Shopify order confirmations include some of this but not all of it in a format a buyer’s AP team can process without manual editing. Automated invoice generation runs via a custom app or a platform like Sufio or Order Printer Pro, which triggers on order creation, fills the invoice template, attaches the PDF to the buyer’s confirmation email, and writes the invoice URL back to the order metafields. For ERP-integrated stores, the invoice generates in the ERP and the PDF URL syncs to Shopify so the buyer can access it from their order page.

5. Customer Account Portal With Invoice Access and Credit Visibility

B2B buyers should not need to contact customer service to find out how much credit they have left or whether an invoice has been paid. A self-service portal covers four things: current available credit balance, open invoice list with due dates, payment history and receipts, and PDF invoice download. This is either built as a Shopify theme extension (for buyers logging into a standard Shopify customer account) or as a headless portal that authenticates against Shopify and pulls financial data from the ERP. The theme extension approach is faster to launch; the headless approach handles more complex account structures. For most mid-market B2B stores, a theme extension with metafield-based data display is the appropriate starting point.

6. Milestone and Installment Payment Support

Milestone billing and installment plans require the platform to treat a single order as having multiple payment events, each with its own amount, due date, and trigger condition. A $200,000 industrial equipment order structured as 30% deposit at placement, 40% at factory completion, and 30% at delivery is a normal commercial arrangement. Shopify’s order model does not support this natively. Implementation uses order metafields to store the full payment schedule, a custom app to monitor trigger conditions (date-based or fulfillment milestone-based), and a payment processor integration such as Stripe or Braintree to capture or invoice each installment at the appropriate time. For high-value capital goods, this capability is not a nice-to-have: it is the mechanism by which the commercial deal structure is honored.

Net Terms Impact: B2B Merchant Data

Source: The B2B Payments Report 2025, Balance

Businesses that increased spend after automated credit limit increase

84%

Average monthly spend growth within 3 months of credit increase

+56%

Existing customers who increased monthly spend with new credit access

+40%

New buyer acquisition after enabling net terms

+38%

Data from merchants enabling net terms and trade credit on their B2B storefronts.

How to Architect a Terms-Enabled Payment System on Shopify Plus

The architecture below covers the five layers of a production-grade B2B payment system on Shopify Plus. These are sequenced in dependency order: each layer builds on the one before it. Teams that try to build the buyer portal before establishing the data layer end up with a portal that displays incorrect or stale information.

credit_limit (the approved maximum) and outstanding_balance (the current unpaid total). These values are the source of truth for all downstream logic. Source them from your ERP or CRM during customer onboarding and keep them current via webhook on every payment received and order confirmed. Without accurate data in these fields, every downstream control is unreliable.credit_limit and outstanding_balance at checkout. If outstanding_balance + cart_total exceeds credit_limit, hide or disable the terms payment option and display a message explaining the situation. Additionally, gate the terms option to buyers with a specific customer tag (for example, b2b-approved) so D2C buyers on the same store never see net terms as a payment option. Also add the PO number field to checkout as a required attribute for tagged B2B buyers.payment_due_date) calculated from the order date plus the net terms period. Use Shopify Flow or a custom webhook handler to schedule three automated email reminders at 7 days before due, 3 days before due, and on the due date. If payment does not post within 5 days of the due date, trigger a credit hold flag on the company metafields, which will block new orders on terms until the balance clears. The hold should be clearable by your finance team with a single admin action.

What Breaks When You Skip This Work

The consequences of running B2B payment terms without proper infrastructure follow a predictable pattern. They start as minor inconveniences and escalate into structural problems as order volume grows. Each of the four failure modes below has a specific downstream cost.

“Payment terms are not a minor feature. They are a signal of trust. The buyer who receives Net 60 on their first large order will remember which supplier made that possible.”

If your Shopify Plus store is running B2B payment terms on manual infrastructure or has outgrown what Shopify provides natively, the team at Optimum7 builds these systems end to end. From checkout logic and ERP integration to buyer portals and milestone billing, see Optimum7’s Shopify development services or contact us to discuss your B2B requirements.

ERP and Accounting Integration: Where the Real Work Lives

For most B2B merchants on Shopify Plus, the most technically complex part of payment term infrastructure is not the checkout logic. It is the integration between Shopify and the systems of record that hold the authoritative financial data. The checkout logic is straightforward once the data layer is right. Getting the data layer right requires a well-designed ERP integration.

NetSuite and Acumatica: Enterprise ERP Integration Patterns

For stores on NetSuite or Acumatica, the integration pattern involves three data flows. First, new Shopify orders push to the ERP as sales orders within minutes of placement, carrying the PO number, line items, customer reference, and applied payment terms. Second, when the ERP records a payment, it fires a webhook or API call to Shopify that updates the customer’s outstanding balance metafield and marks the relevant order as paid. Third, when the ERP generates an invoice PDF, the document URL writes back to the Shopify order metafields so the buyer can access it from their account without contacting support. Celigo’s Shopify-NetSuite connector covers most of this out of the box; Acumatica integrations typically require more custom connector work.

QuickBooks and Xero: Mid-Market Integration Patterns

For mid-market B2B stores using QuickBooks Online or Xero, the same three-flow pattern applies, but the tooling is lighter. Apps like A2X or OneSaas handle basic order sync, though they typically do not support the bidirectional balance updates needed for credit limit enforcement without custom extension. Stores that need credit metafield updates from QuickBooks will typically need a custom sync layer: a serverless function or lightweight middleware that listens for payment events in QuickBooks and updates the corresponding Shopify customer metafields. The implementation is simpler than a full ERP integration but still requires thoughtful error handling for sync failures and reconciliation edge cases.

Payment Processors for Milestone and Installment Billing

Milestone and installment payment logic requires a payment processor that supports future charge scheduling or separate invoice issuance. Stripe handles both well: the PaymentIntents API supports off-session charges at scheduled dates, and Stripe Invoicing handles the invoice-and-pay-later workflow. Braintree provides similar capabilities with better support for certain international payment methods. The integration stores a customer’s payment method on the processor at order time, writes the full payment schedule to Shopify order metafields, and fires charges or sends invoices at each milestone trigger. For complex structures, the processor integration and the Shopify order model stay loosely coupled through order metafields, which avoids the fragility of trying to map multi-event payment logic onto Shopify’s single-transaction order model.

Building the Buyer Portal Your Finance Team Will Stop Fielding Calls About

The buyer portal is the front-end piece that turns backend infrastructure into a visible experience for your customers. A well-built portal eliminates a specific category of support volume: calls and emails from buyers asking about their current balance, requesting invoice copies, or asking when a payment they submitted was applied. Every one of those requests is addressable with a self-service portal displaying live data from the ERP sync.

The four things every B2B buyer portal needs are: a current available credit display (so buyers know before adding items to cart how much room they have), an open invoice list with individual due dates and payment statuses, a full payment history with receipt download for each paid invoice, and a searchable order history that connects orders to their corresponding invoices. Optional additions that are high-value for larger accounts include a credit limit increase request form, a dispute submission flow, and a multiple-buyer account structure with role-based access (buyer vs. finance vs. read-only).

For implementation, the choice between a theme extension and a headless portal comes down to account complexity. If your B2B buyers are single contacts purchasing for a single entity, a theme extension on Shopify’s customer account pages is sufficient and faster to build. If your buyers represent organizations with multiple contacts, different purchasing roles, and subsidiaries with separate credit limits, a headless portal with custom authentication handles the hierarchy better. Both approaches should pull live data from the ERP-synced metafields rather than storing financial state in Shopify directly. For additional technical context on building API-safe infrastructure on Shopify Plus, see Shopify Plus API infrastructure for industrial-scale operations.

Related Reading

If you are building out a complete B2B purchasing infrastructure on Shopify Plus, these posts cover the adjacent systems that connect with payment term architecture:

- Building a custom PO management system in Shopify Plus: how to handle PO creation, approval routing, and order matching end to end.

- Step-by-step guide to enabling ACH payments on Shopify Plus for B2B stores: how to set up ACH as a payment method, configure approval flows, and integrate it with your payment terms to support large-volume B2B transactions efficiently.

- B2B ecommerce strategy for mid-market and enterprise: channel design, buyer experience, and conversion optimization for B2B storefronts.

Frequently Asked Questions

Does Shopify Plus support Net 30 payment terms natively?

Shopify Plus includes basic net payment terms (Net 15, Net 30, Net 60, Net 90) assigned at the company location level. Buyers can select these at checkout. However, Shopify Plus cannot track when payment is due, send automated reminders, block orders from customers with overdue balances, or enforce per-customer credit limits at checkout. Those capabilities require custom development or a third-party terms platform.

How do you enforce credit limits at checkout on Shopify Plus?

Shopify Plus has no native credit limit enforcement at checkout. To enforce limits, you store the approved credit limit and current outstanding balance in customer metafields, then use a Shopify Function to compare available credit against the cart total at checkout. If the cart would exceed available credit, the terms payment option is hidden or disabled. This logic must be built as a custom app or installed via a third-party B2B payment platform.

What is the difference between draft orders and net terms on Shopify Plus?

Draft orders are internal records created by Shopify admin staff, typically used to generate invoices manually and email payment links to buyers. Net terms are a payment method available at checkout that allows buyers to complete orders without immediate payment. Draft orders work for low-volume programs; net terms built via a checkout extension scale properly. For merchants handling more than 50 B2B orders per month, net terms at checkout outperform draft order workflows in reliability and buyer experience.

Can Shopify Plus integrate with NetSuite for B2B payment term tracking?

Yes, but the integration requires custom development or middleware platforms such as Celigo, Boomi, or a custom API connector. The integration syncs order data, payment status, credit limits, and account balances between Shopify Plus and NetSuite in near real time. NetSuite remains the system of record for accounts receivable while Shopify Plus displays current credit availability to buyers and internal teams at checkout.

What apps support B2B payment terms on Shopify?

Third-party platforms that extend Shopify Plus with net terms and trade credit functionality include Resolve Pay, Balance, Apruve, and Behalf. These tools typically provide buyer credit assessment, automated net terms at checkout, invoice generation, and collections workflows. The right choice depends on whether you need full white-label control, deep ERP integration, or a managed credit solution. Custom development is also an option for stores with proprietary credit logic or complex ERP requirements.

How do you build a purchase order workflow in Shopify Plus?

A PO workflow on Shopify Plus involves adding a PO number field to checkout via a checkout extension, storing the reference in order metafields or attributes, routing orders through a custom app for internal approval if required, and generating invoices post-approval. The PO number syncs to the ERP so finance can match it to incoming payments. Native Shopify Plus has no built-in PO approval routing; that logic requires custom development.

What is milestone billing and can Shopify Plus handle it?

Milestone billing splits a total order value into multiple payment events tied to project stages: for example, 30% deposit at order placement, 40% at production completion, and 30% at delivery. Shopify Plus has no native support for milestone billing. This requires a custom app that stores the payment schedule in order metafields, monitors trigger conditions, and integrates with a payment processor such as Stripe or Braintree to capture or invoice each payment at the appropriate stage.

How do B2B buyers access invoices on Shopify Plus?

By default, Shopify Plus shows buyers their order history in the customer account area but does not display open invoice balances, payment due dates, or downloadable PDF invoices clearly. Most B2B stores build a custom buyer portal, either as a Shopify theme extension or a separate web app, that pulls invoice data from the ERP and displays open balances, due dates, and payment history. This eliminates the support calls buyers make when they cannot find their invoice or do not know their current balance.

What does a properly built terms-enabled checkout look like on Shopify Plus?

A proper terms-enabled checkout shows the buyer their current available credit, displays the payment terms assigned to their account (for example, Net 30 due ), hides the terms option if the cart exceeds their credit limit, and lets them submit the order without immediate payment. After the order is placed, an invoice generates automatically, syncs to the ERP, and the buyer receives a confirmation email with the invoice and payment due date included.

How long does it take to build custom B2B payment term infrastructure on Shopify Plus?

A basic net terms checkout with credit limit enforcement takes roughly 4 to 8 weeks of development. Adding ERP integration, a buyer portal, milestone billing, and PO approval workflows can extend the timeline to 12 to 20 weeks depending on system complexity. Using a purpose-built platform such as Resolve Pay or Balance alongside Shopify Plus reduces custom development to integration and configuration work, shortening the launch timeline considerably.

About the author: Duran Inci is the CEO and Co-Founder of Optimum7, an ecommerce development and digital marketing agency. He helps mid-market and enterprise brands scale revenue through conversion optimization, SEO, and custom ecommerce solutions.